APAC prime office rents finally record first quarterly increase in three years

Rents inched up by 0.2% in Q2 2025.

Prime office rents across the Asia-Pacific region registered their first quarterly increase in close to three years, rising 0.2% quarter-on-quarter in Q2 2025, according to Knight Frank's Asia-Pacific Office Highlights report.

“The quarterly gain signals a potential stabilisation after a prolonged downturn driven by weakness in the Chinese mainland market. The other markets were largely stable or slightly impacted by the tariff war during the quarter, as many did not consider the tariff rates permanent.”

Here are some key highlights from Knight Frank’s report:

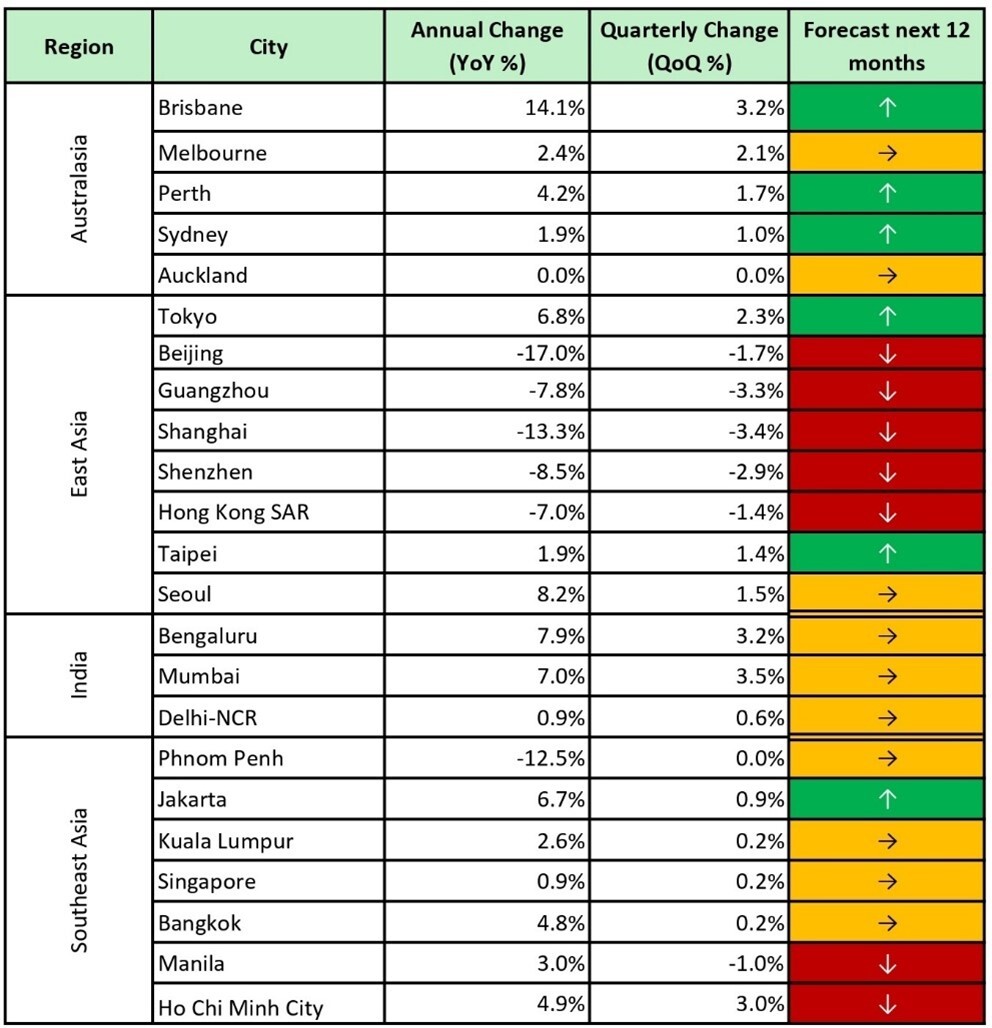

- 17 out of 23 monitored cities reported stable or increasing rents year-on-year

- Brisbane leads growth at 14% year-on-year amid strong premium asset demand on Australia's Eastern Seaboard

- Hong Kong pricing opportunity deepens: Hong Kong office rents have decreased by 34% since the Q4 2019, making it attractive to those occupiers looking to set up regional headquarters.

- Chinese mainland stabilises with rental declines moderating to 2.9% from 4.3% in Q1

- Indian markets hit highest Q2 volumes with 1.2 million sqm leased across three major cities, up 20%, driving rental growth acceleration to 4.5% year-on-year

- Tokyo overtakes Seoul to register the lowest vacancy rate due to limited new supply

Here’s more from Knight Frank:

Hong Kong offers significant cost advantages for companies seeking office space. Rentals have fallen substantially since Q4 2019, making them particularly attractive to occupiers. The premium Hong Kong offices once held over Singapore has narrowed sharply, from 105% in Q4 2019 to just 24%. This reduced gap creates attractive cost savings for companies looking to establish regional headquarters in Hong Kong.

Tim Armstrong, global head of occupier strategy and solutions, says, "As global disruption becomes the status quo, occupiers are rethinking real estate not just as a place to work, but as a strategic platform for growth. They want flexibility to pivot with speed, functionality that supports evolving business models, and resilience built into every square foot to weather what's ahead. Tenant activity for relocations is likely to remain modest as occupiers turn selective, shifting focus towards more holistic and dynamic strategies amid a flight-to-functionality."

Jane Street's major Hong Kong lease signals market confidence

US quantitative trading firm Jane Street struck one of Hong Kong's largest prime office leases in recent years, securing over 220,000 square feet as the territory capitalises on its position as a leading centre for Chinese mainland firms seeking offshore funding. The deal demonstrates Hong Kong's strategic importance despite ongoing US-China trade tensions.

Christine Li, head of research, Asia-Pacific, Knight Frank adds, “Capital flows and corporate strategies are being reshaped as Trump's policies shift global dynamics and accelerate US-China decoupling. Chinese mainland companies are now favouring Hong Kong over the US as a listing destination, while global investors are increasing their presence in the region to tap investment opportunities and the expansion in private capital. Several financial firms have sealed high-profile leases in Hong Kong in recent months. At the same time, we have also observed an uptick in enquiries from Chinese companies looking to expand in Southeast Asia. The region's office markets are well placed to capitalise on this new trend, offering firms a strategic platform to continually tap growth opportunities while navigating rising geopolitical tensions.”

This shift is driving mainland Chinese and Hong Kong firms to explore Southeast Asia for expansion amid ongoing trade tensions, with companies keen to tap Singapore's bourse for regional market entry. Alternative investment manager Quantedge Capital exemplifies this trend, expanding its Singapore footprint to a 30,000 square foot space in Capital Tower. Singapore remains a regional financial hub, with plans to boost the local stock exchange through a S$5 billion (US$3.9 billion) government programme.

India achieves its strongest Q2 performance

India's three largest office markets – Bengaluru, Mumbai, and Delhi-NCR – collectively leased 1.2 million square meters in Q2 2025, marking the highest second-quarter volume on record and representing a 20% increase from the previous year. This growth drove rental growth acceleration to 4.5% year-on-year with strong business sentiment despite geopolitical headwinds.

Bengaluru continued to lead, with 1.7 million square meters leased in the first half of 2025, surpassing the full-year 2024 volumes. Delhi-NCR also achieved new records, with 700,000 square meters leased in H1 2025.

Global Capability Centres (GCCs) maintained their position as the largest occupier segment, with third-party IT service providers doubling their market share from 10% in the same period last year to over 20% in 2025.

Chinese mainland shows signs of stabilisation

The rental decline across the Chinese mainland's tier-one cities moderated significantly in Q2 2025, with prime rents softening 2.9% quarter-on-quarter compared with 4.3% in Q1 2025. Policy support measures have helped stabilise vacancy rates and moderate rental declines, particularly in Beijing.

Leasing demand in Shenzhen was driven by technology, media, and telecommunications (TMT) and professional services firms. Most recently, a division of Huawei Technologies secured 10,000 square meters in a prime office tower, reflecting the government's drive to promote technology self-sufficiency.

Brisbane leads as Tokyo tightens

Brisbane continued to lead rental growth across the region, rising over 14% year-on-year, driven by strong demand for premium-grade assets as competition for high-quality spaces intensifies on Australia's Eastern Seaboard markets.

Tokyo overtook Seoul to have the region's lowest vacancy rate. Limited new supply kept vacancy rates low, while Seoul's vacancy rates increased marginally due to new deliveries and delayed leasing negotiations during South Korea's elections.

Outlook remains cautious

Despite the positive momentum, the report cautions that it remains too early to call a definitive bottom, as conditions remain volatile. The expiration of Trump's trade deadline, now delayed to August, continues to cloud visibility and may weigh on leasing momentum in the short term.

Forecast for the next 12 months

Advertise

Advertise