Hong Kong office rents now 30% below 2019 peak levels

Rents are expected to continue on this downward trend for the coming months.

According to a Savills report, the third quarter saw further rental declines across all districts in Hong Kong ranging from a relatively modest -0.4% in the Western Corridor (Cheung Sha Wan / Kwai Chung / Tsuen Wan) to -3.4% in Island South.

From their previous peak in 2019, rents are now down by around 30% with further falls expected over the next 12 months.

Here’s more from Savills:

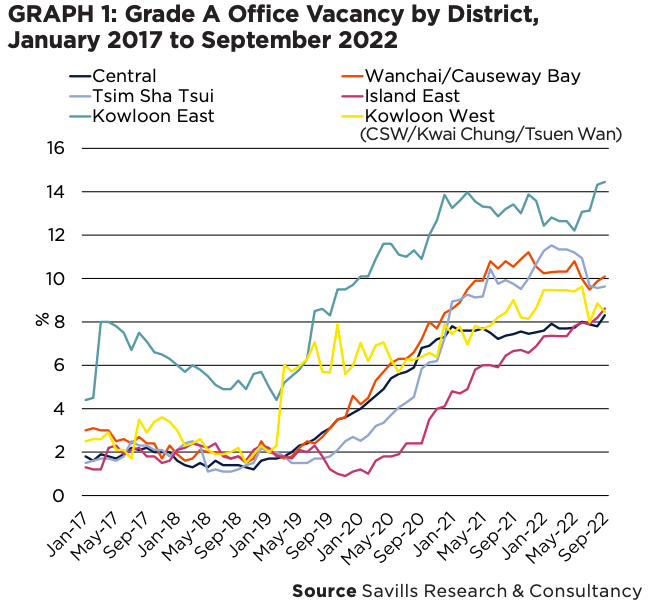

Vacancy now stands at 10.2% (6.5 million sq ft net) with notable pockets of availability appearing in Kowloon East (14.4% / 1.9 million sq ft net) and Central (8.3% / 1.3 million sq ft net). In some districts vacancy is close to or above GFC levels from 2009. Set against a background of slowing economic growth and ongoing COVID restrictions, we expect demand to remain lacklustre over the final quarter of the year and vacancy can be expected to tick up into next year as new supply is added to the market.

In a regional context it is worth noting that Hong Kong is still an expensive place to do business compared with many of our neighbouring cities. At least two cost of living surveys rank the SAR number one in the region, ECA International and Mercer, while Savills own data on the cost of renting prime-prime offices put Hong Kong well ahead of its closest rival, Tokyo.

The effective closure of the border with Mainland China has cooled demand from mainland businesses which, though remarkably resilient through the pandemic, is still below 2018 levels. Prime movers are businesses involved in private funds or asset management, securities, banking, real estate and insurance.

Demand remains heavily core focused and in Central Mainland businesses now occupy around 25% of all Grade A office space while that figure is significantly higher in Sheung Wan at 35%. Buildings with the highest PRC occupancy are all mainland owned and include CCB Tower, Bank of China Tower, Agricultural Bank of China Tower and CITIC Tower.

Looking ahead, besides mainland businesses, demand is emerging (modestly) from several other areas including ESG firms, Fintech, cryptos and NFTs / art auctioneers, medical services, government and public bodies, and private members clubs. We are still seeing take-up from serviced office operators but after aggressive growth since 2021 this has fallen back recently.

One major hurdle for tenants looking to relocate is cost as typical fit-outs now average around HK$1,000 per sq ft plus reinstatement of HK$200 per sq ft making a three year lease term hard to justify. Landlords are responding slowly by offering larger rent free periods or even CAPEX subsidies in some rare cases. For smaller tenants, fully fitted units are particularly appealing in today’s market.

Advertise

Advertise