What does recovery look like for Tokyo’s office submarkets?

Savills says submarkets that saw larger corrections will continue to have hard times ahead.

Tokyo’s office market has seen improving prospects over the recent quarters. With the impacts of the pandemic waning and the society slowly going back to normal, Tokyo’s office vacancy rates are stabilising and the rental corrections are moderating.

According to a Savills report, the average market rent of Grade A offices stayed flat in Q3/2022 for the first time since Q2/2020. With the market average rent having reversed back to the levels seen in 2017, tenants seem to be finding current rents reasonable.

Here’s more from Savills:

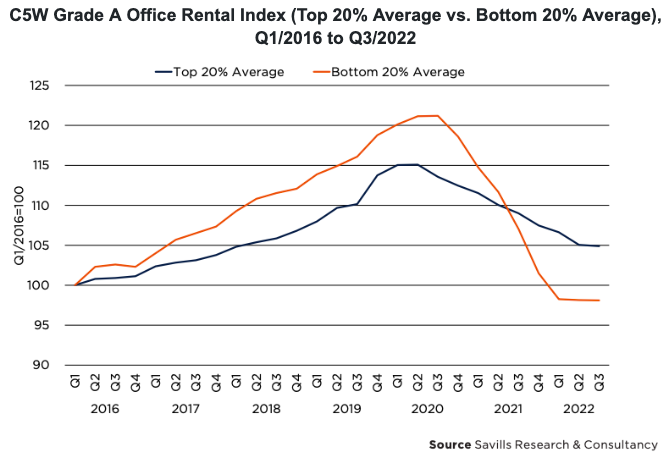

Nonetheless, we expect future recovery to be uneven across the market. The below graph suggests that properties in the bottom 20% in terms of rental levels have suffered disproportionately more than the top 20%. It is especially interesting to see that the former is now below 2016 levels while the latter has maintained 2018 levels. This might indicate that some lower-rent properties have been caught in price competition.

Going forward, we believe that submarkets and properties that saw larger corrections will continue to have hard times ahead. In fact, while good quality properties with convenient access have been able to attract tenants who find their current rental levels reasonable, other properties with relatively low rents are struggling to fill space even with aggressive discounts and prolonged free rental periods. These properties were able to attract tenants when the market was extremely tight, but their allure of affordability has faded in the current market environment where quality offices can be secured at reasonable rents. This explains how the rental level of the bottom 20% plunged much more than the top 20% in the graph.

At the submarket level, this suggests that prime submarkets such as Marunouchi and Shibuya are likely to exhibit steady recovery as the demand for highly regarded office towers in these areas will likely continue to be strong. This is particularly true for Grade A offices around Shibuya station, which have very tight vacancy rates and are likely to lead the recovery. Indeed, many office towers around the station have not reduced rents for over a year, and pre-leasing for the Sakuragaoka Project appears to be going smoothly.

On the other hand, the submarkets with older office buildings will likely lag others in recovery. Specifically, the submarkets such as Shinjuku and Shinagawa & Osaki have seen larger rental corrections primarily due to their older office stock, and might take more time to return to the pre-pandemic level.

Shinjuku’s redevelopment has lagged other submarkets, as many office towers in the submarket were built between the 1970s and 1990s. While they go through regular renovations, Shinjuku’s relative competitiveness appears to have dwindled with other submarkets seeing new, state-of-the-art towers built in recent years.

Shinagawa & Osaki also has a relatively aged stock with many built in the 1990s and early 2000s. To be sure, these office buildings are not necessarily old. However, the difference for Shinagawa & Osaki is that the submarket was formed relatively recently, and there are no Grade A office towers that were built before the 1990s.

As a result, the submarket has not seen as many new offices since its buildings are not aged enough to be redeveloped, making the average age relatively high. That said, several development projects are underway around Shinagawa station and Takanawa Gateway station. Those large-scale mixed-use projects could provide a boost for the area’s long-term growth.

Putting everything together, we continue to expect a gradual recovery for the overall Tokyo market over the next few years. As discussed above, while stronger properties should see faster recovery, weaker ones will likely drag the market down, which together will likely result in mild recovery for the Tokyo office market as a whole.

Specifically, actual vacancy rates have been higher than we expected partially because pre-leasing for new office towers completed this year was slower than our initial assumption. Additionally, recent developments in the global economy including the prolonged war in Ukraine, persistent inflation, and global quantitative tightening have prompted us to lower the rental growth expectation in 2024.

Nonetheless, Japan’s economy is faring relatively better than its global peers with inflation remaining at manageable levels. Furthermore, corporate performances are still improving albeit at a modest level, and active pre-leasing for supply in 2023 also bodes well for next year.

Advertise

Advertise