Why APAC logistics rental growth slowed to a mere 0.2% in 2024

Rental growth was at 7% in 2023.

According to Knight Frank’s Asia-Pacific H2 2024 Logistics Highlights report, Asia Pacific’s logistics sector is at a crossroads amid geopolitical uncertainties and evolving market dynamics.

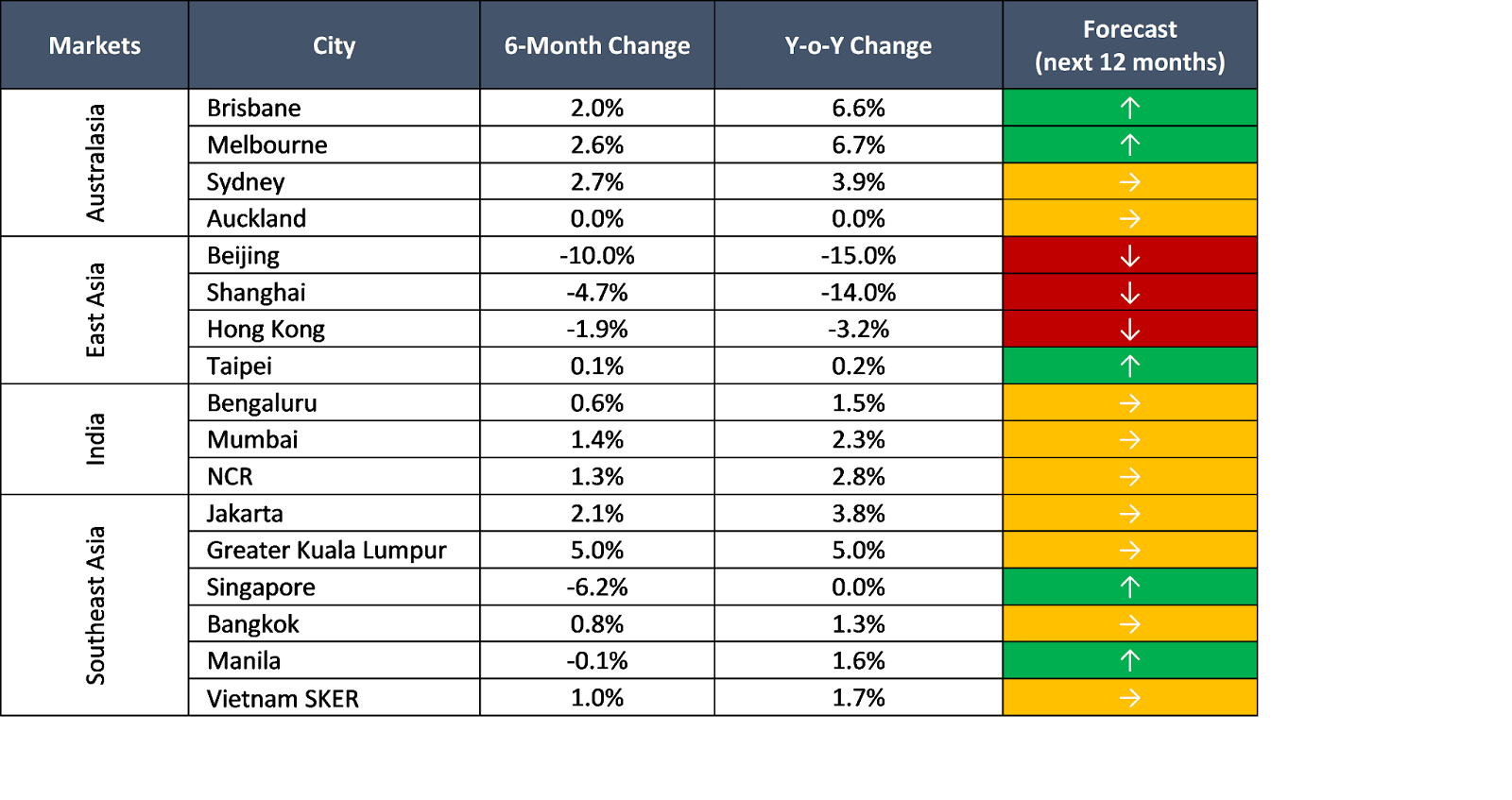

While 14 of 17 tracked cities recorded stable or increasing rents year on year in H2 2024, the report unveils a stark contrast in regional performance. Overall rent growth for logistics spaces in Asia-Pacific slowed to just 0.2% in 2024, down sharply from 7% in 2023 and 2% in the first half of 2024.

Here's more from Knight Frank:

This deceleration, however, masks significant market variations across the region. Markets in the Chinese mainland face headwinds, with Beijing and Shanghai experiencing 14% to 15% rent plunges due to a substantial development pipeline, which is expected to reach over 4 million sqm. The considerable development pipeline will lift vacancy rates in both cities to nearly 30% in 2025, exerting considerable downward pressure on rents.

In contrast, Melbourne emerged as a top performer with 6.7% growth, driven by land scarcity in key submarkets. Southeast Asian markets show resilience, with Greater Kuala Lumpur leading half-yearly rental growth of 5% as the completion of higher-quality industrial properties lifted rents.

Looking ahead, the potential for increased tariffs under a second Trump administration could accelerate the realignment of global supply chains, both within Asia-Pacific and between regions.

Tim Armstrong, global head of occupier strategy and solutions, Knight Frank, says, “As the world braces for Trump 2.0, the realignment of supply chains is likely to gather pace in response to planned tariff increases. China-plus strategies, consequently, are expected to take on added urgency as manufacturers focus on further diversifying bases in Southeast Asia and India, strategically leveraging these locations to friend shore operations. Occupiers will have to tread a strategic tightrope, focusing on cost management while selectively evaluating their logistics footprint. This emphasises logistics hubs that are well-connected to major trade routes. The evolving geopolitical landscape and preference for modernised distribution facilities are expected to continually drive demand for well-located, efficient prime logistics spaces in the region."

The Asia-Pacific logistics sector is expected to maintain a delicate balance in 2025 despite market fluctuations. Occupiers will likely focus on optimising their existing footprints and working through excess capacity, which should help stabilise demand-supply dynamics.

Prime logistics spaces are anticipated to see continued healthy demand, with leasing volumes keeping pace with new supply. As a result, regional vacancy rates are forecast to remain largely stable, supporting moderate rent growth of up to 2%.

Christine Li, head of research, Asia-Pacific, Knight Frank adds, “A flight-to-quality trend will remain supportive of demand for new logistics spaces in the region, as occupiers continue to plan for supply chain contingencies and optimise the use of technology in their operations. The manufacturing sector is also emerging to be a key source of demand, particularly in high-growth, strategic sectors such as electric vehicles and electronics, as the need for specialised supply chains will reshape the region's trade and logistics landscape. Aside from Chinese mainland markets, where excess capacity will continue to depress rents, those in the rest of the region will be supported by more balanced demand-supply dynamics. At the same time, the delivery of new premium facilities in the region's emerging markets will also prop up average rents.”

Advertise

Advertise