Singapore private home launches in Q2 hit record lows since Q4 2022

Launches slumped by 73.3% to 634 units.

Savills Research shares that the number of new private residential launches in the second quarter has contracted in the second quarter – the lowest since Q4 in 2022. This marks a 73.3% decline on a yearly basis.

After a rebound in Q1/2024, the number of units launched contracted in Q2/2024, more than halving from 1,304 units to 634 units, the lowest since Q4/2022 when 504 units were launched.

The contraction is due to a lack of larger-scale developments being launched. There is also a slump in units launched in the Outside Central Region (OCR) - 1,060 units in Q1 to 126 units in Q2 – the lowest since Q2 last year.

Launches in the two other market segments recorded quarterly increases. In the Core Central Region (CCR), the number of launched units surged from just 20 in Q1 to 259 units in Q2. In the Rest of Central Region (RCR), the number of launched units grew by 11.2% quarter-on-quarter (QoQ) to 249 units.

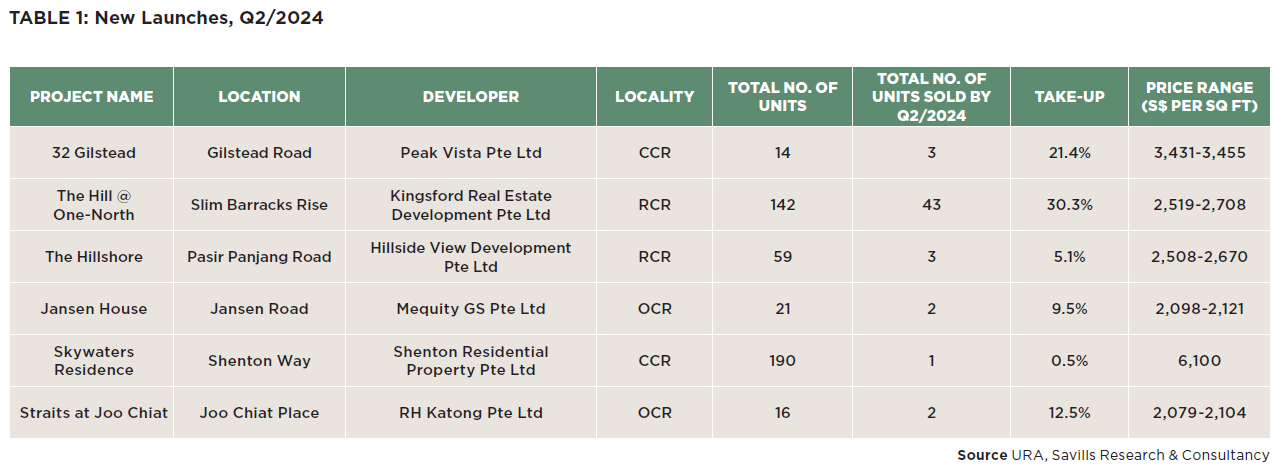

Developments launched were also generally smaller in scale, which may have led to slower take-up rates. The take-up rate of the six new launches in Q2 ranged approximately between 0.5% and 30%, similar to most of the new launches in Q1. The development with the highest take-up in the quarter was The Hill @ One-North with a take-up rate of 30.3%. (see Table 1)

Secondary sales have rebounded in the second quarter, increasing 36.7% QoQ, the highest since Q2/2022 and comes after three consecutive quarters of decline. Secondary sales in all three market segments registered quarterly increases, with the largest growth in CCR at 47.1% QoQ. Secondary sales in RCR and OCR grew 35.7% and 34% QoQ respectively.

Apart from the smaller number of new launches in Q2, the large disparity in prices between new sales and secondary sales may have led homebuyers to turn to the secondary sales market. The price gap between these two markets across the three market segments ranged from 44.7% to 61.2%, with the CCR recording the largest price difference of 61.2%. For example, a resale unit price of S$2,044 psf in the CCR was much lower than the new sale unit prices in both RCR and OCR, at S$2,615 psf and S$2,107 psf, respectively.

George Tan, Managing Director, Livethere Residential, Savills Singapore says, “We are seeing higher sales in the resale market currently because less projects were launched. However, we expect sales of new developments to pick up in the second half of this year, especially when larger-scale projects will be launched across all the three market segments and the anticipation of lower interest rates.”

Alan Cheong, Executive Director, Research & Consultancy, Savills Singapore comments, “While there appears to be some indigestion in the new sales market, developers may not have the flexibility to lower prices. Unless the project has exceptional attributes, first week new sales would likely hover around 25% to 30%.

“Moving forward, we may see a new trend where projects may experience sales clustering around the start of launch and another as it nears completion. Currently, we are maintaining our forecast for prices to remain flat with some upside bias in 2024.”

Advertise

Advertise