Hong Kong prime office rents record slowest rate of decline since 2019

Q3 rents slipped 1% in Hong Kong, whilst the rest of APAC markets saw uneven recovery.

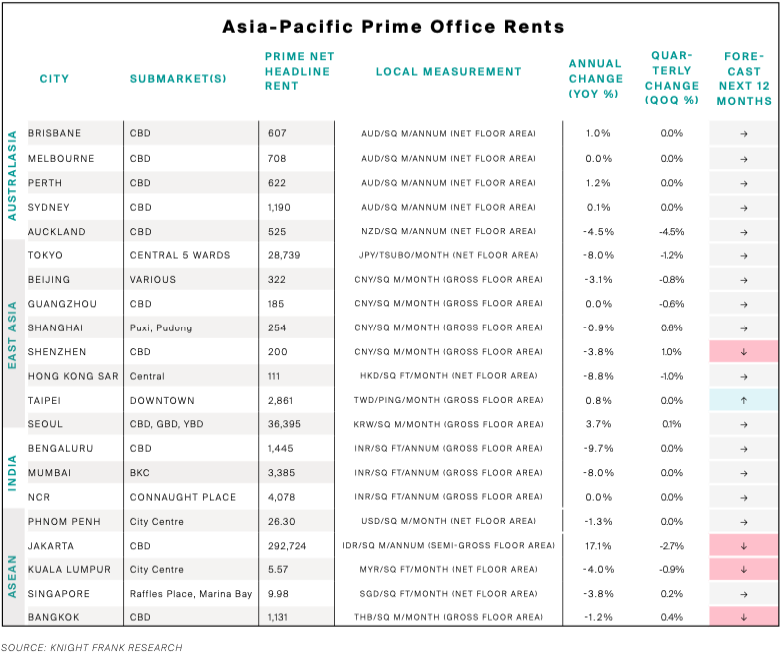

Knight Frank’s latest Asia Pacific Office Rental Index declined 0.3% QoQ and 3.1% YoY in Q3, confirming the continuous rental decline deceleration across the region since the beginning of the year.

Overall vacancy rates remained stable and the region saw uneven recovery across different markets. “The final stretch of 2021 should see continued stabilisation of prime office rents, as COVID restrictions begin loosening over time. Leasing activity is also expected to pick up moderately, and we maintain our expectations that the rate of rental decline will continue to decelerate across the region towards the start of the next year,” adds Knight Frank.

Here’s more from Knight Frank:

Optimism at the start of the year was marred by multiple resurgences of COVID-19 across the region. The new strains of the virus have proven significantly harder to contain, resulting in many markets re-tightening movement restrictions. The management of the pandemic has varied greatly across different markets, and growth forecasts for the region have been lowered for 2021.

For Q3 2021, Knight Frank’s AsiaPacific Prime Office Rental Index fell 0.3% quarter-on-quarter (QoQ). On an annual basis, the overall index is down 3.1% year-on-year. Overall vacancy remains unchanged, as the market is bifurcated, and improvements in takeup in some markets are cancelled out by negative net absorption in others.

The expected pipeline of supply in Asia-Pacific for 2022 is 9.7% of total available stock in the market, which is not significantly elevated from 8.8% in Q2 2021. Therefore, we are not expecting significant supply-side pressures on rents and occupancy during the following quarters. The final stretch of 2021 should see continued stabilisation of prime office rents, as COVID restrictions begin loosening over time for more markets. However, recovery would likely be uneven, with the pandemic being protracted in some places.

Nevertheless, leasing activity should begin to pick up moderately, as conditions normalise gradually. We maintain our expectations that the rate of rental decline will continue to decelerate across the region towards the start of the next year.

Singapore’s prime office market recorded growth for the first time after 6 consecutive quarters of decline, with prime rents rising by 0.2% QoQ in Q3 2021. While case numbers have been on the rise since August, the office market remains relatively unfazed as the drive for vaccination has reached most of the population. With expectations for economic recovery for the full year of 2021 as well as improving employment, office rents should continue to recover modestly in Q4.

Office rents across Australia’s major capitals remained stable in Q3 2021, with Sydney, Melbourne, Perth and Brisbane all seeing no change in net headline rents. Despite that, vacancies have been rising off negative net absorption throughout the year with consecutive and repeated movement restrictions due to the prolonged state of the pandemic. Sydney, the largest office market in Australia, is seeing much higher leasing activities in the year so far thanks to a rebound in the economy, recording 20,586 sqm of net absorption during the period. While 180,000 sqm of new development stock is currently under construction, 60% of these schemes have already been committed, and thus will not be expected to put significant pressures on the market by time of completion.

While rents in Hong Kong SAR have been declining since 2018, the market has seemingly turned a corner in Q3 2021 with a rebound in leasing momentum. Prime office rents fell by 1.0% QoQ in Q3 2021, the slowest rate of decline since Q2 2019. The lower rents have prompted occupiers to return to the market, leading to more leasing activities. With demand re-emerging, the vacancy rate of Hong Kong's Central grade-A office market is gradually decreasing. We expect rents to stabilise across Hong Kong’s major locations, particularly among higher quality buildings that still have lower asking rents in Q4 2021.

Advertise

Advertise