Thailand warehouse takeup rate hits record highs of over 600,000sqm in H1 2024

This sharp increase was driven by the influx of new supply.

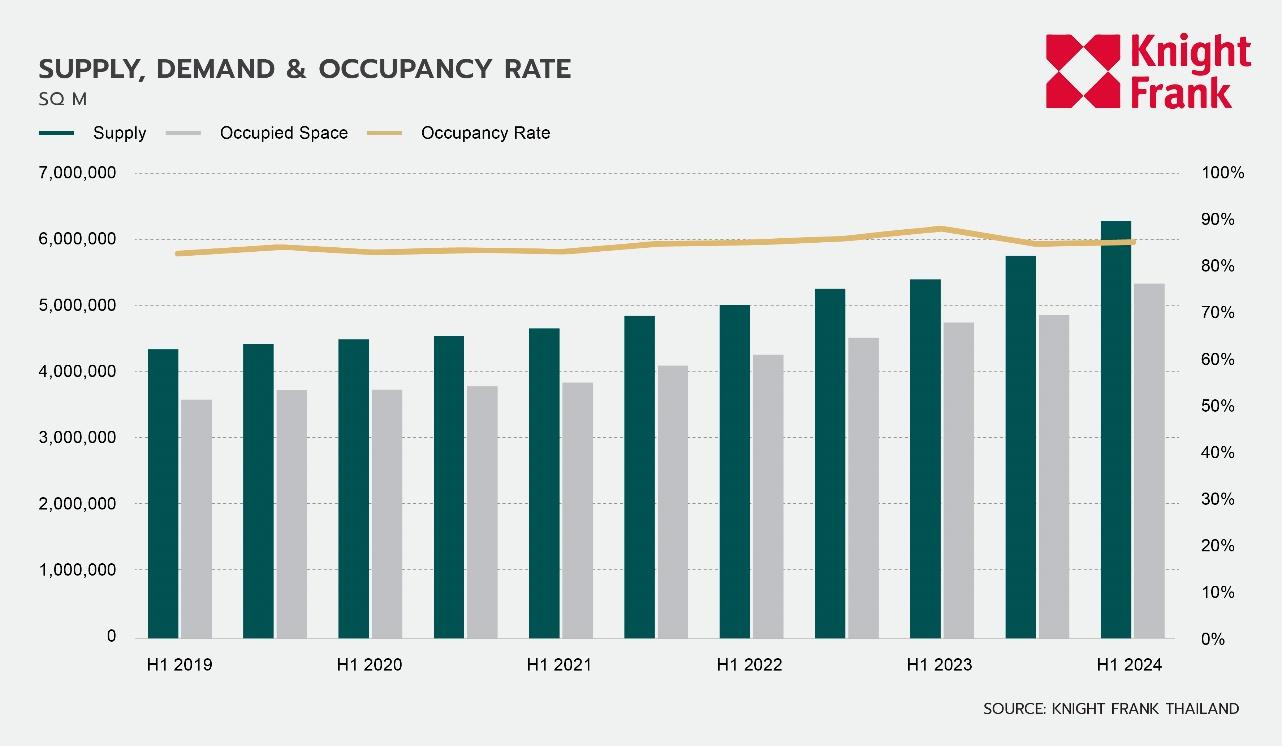

According to data from Knight Frank, in the first half of 2024, the warehouse market saw substantial growth in both supply and occupied space. Supply levels surpassed 6.27 million sq m, while occupied space rose to 5.33 million sq m, reflecting strong demand across the market.

However, occupancy rates declined slightly to 85.0%, lower than the previous year, primarily due to the influx of new supply.

Here’s more from Knight Frank:

Despite this, the market continues to absorb new supply effectively, with strong demand from key sectors such as e-commerce, automotive, and electronics driving the ongoing strength of the logistics property market. Meanwhile, the automotive industry saw a surge due to the expansion in EV manufacturing and related infrastructure, aligning with global sustainability stimulation.

In contrast, demand in the garments, chemicals, and construction materials sectors declined. Investors from China, the Netherlands, South Korea, Japan, and Hong Kong have shown strong confidence in Thailand’s logistics sector. Their contributions go beyond financial support, bringing in cutting-edge technologies and innovative warehousing solutions to transform the industry, particularly in transportation and cargo handling, which accounts for a significant share of foreign investment in the logistics market.

Following this demand, the take-up rate in H1 2024 exceeded 600,000 sq m, marking the highest level in recent years. This sharp increase was driven by the influx of new supply, particularly built-to-suit developments designed to meet the specific needs of growing sectors. The rapid absorption of these spaces highlights the market’s ability to accommodate new stock effectively, further demonstrating the resilience and growth potential of Thailand’s logistics property sector.

In the Bangkok Metropolitan Region (BMR), occupancy levels reached 89.6%, a slight decrease of 0.2% pts H-o-H and a 2.5% pts Y-o-Y decline. Despite this, the BMR continues to lead with the highest share of occupied space at 2.5 million sq m, driven by ongoing demand from the e-commerce and logistics sectors. The regions also posted the highest net absorption of 222,452 sq m in H1 2024.

The Eastern Seaboard saw a rise in supply in H1 2024, which led to the absorption of a substantial 191,909 sq m of warehouse space, reflecting strong demand. The region’s occupancy rate increased by 1.4 percentage points H-o-H to 78.8%, primarily driven by the influx of new supply. This increased available space positions the EEC to accommodate future growth and demand in the logistics sector.

Meanwhile, the Central region showed steady performance with occupancy at 86.9%, down by 0.2% pts H-o-H but up by 0.6% pts Y-o-Y. The region recorded a net absorption of 47,141 sq m in H1 2024, with a total occupied space of 900,442 sq m, indicating balanced supply and demand dynamics.

Despite the slight decline in occupancy rates, the market remains fundamentally strong. The additional stock is being steadily absorbed, reflecting sustained demand across various sectors. The lower occupancy rate is not a sign of weakening demand but rather the result of a faster expansion in supply.

Advertise

Advertise