Top 10 APAC cities by industrial investment activity in 2020

Seoul, Tokyo, and Sydney grab the top three spots.

According to Colliers, aggregate transactions of industrial and logistics property reached USD34.5 billion in 2020. This was 2.4x the 2011 total of USD14.5 billion, implying average annual growth of 10% over the last decade.

The appearance of new manufacturing hubs should drive further growth in manufacturing property deals, while expansion in the last mile and cold chain market segments should drive further growth in logistics property deals.

Here’s more from Colliers:

Australia, Japan, Hong Kong and Singapore are often perceived as the mature markets in the sector. However, some of these markets are still growing strongly. Notably, Australia posted an 18% increase in deal volumes in 2020.

Transactions in China and South Korea have grown at average annual rates of 18%-19% over the past decade. However, both markets saw further growth in 2020: 58% for China and 12% for South Korea. We believe that this high growth can continue.

The “others” category in the chart below includes India, Thailand, Indonesia, Vietnam and New Zealand. Deal volumes in these markets are still small, at USD1.7 billion in 2020. However, these markets may well have the greatest growth potential looking forward.

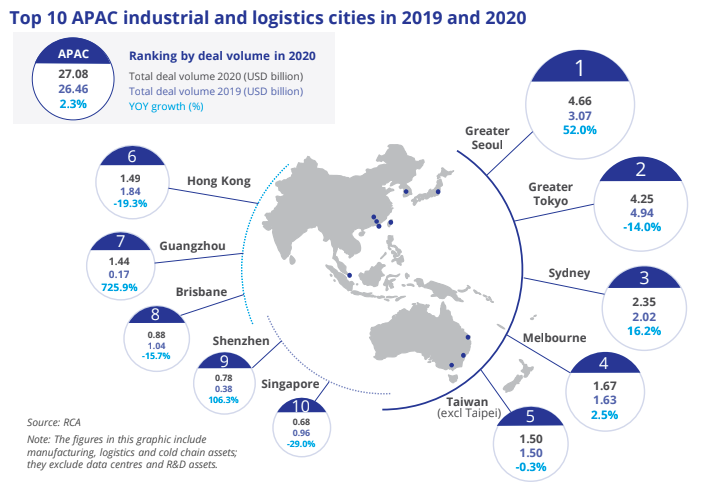

By city, Greater Seoul (Seoul, Incheon and the surrounding cities) in South Korea led investment activity in the industrial and logistics sector in APAC in 2020. This area posted 52% growth in deal volumes to USD4.66 billion.

Ranking second in APAC in 2020 was greater Tokyo, albeit with a 14% YOY drop in deal volumes to USD4.25 billion.

Sydney and Melbourne ranked third and fourth place among APAC cities, with growth in deal volumes of 16% and 3%, respectively.

Advertise

Advertise