What’s the most sought-after property sector in Japan?

Valuations in this sector have reached record highs.

Recent corporate performance alongside economic recovery suggests better times ahead. According to Savills, this growth comes from a return in demand for electronics and automobiles in response to COVID-19 and an increased push for digitalisation. That said, the slow pace of vaccinations in Japan is likely to keep personal consumption depressed throughout 2021 and any economic recovery to pre-COVID levels should be achieved in 2022 or later.

Here’s more from Savills:

The national unemployment rate remains stubbornly low, at 2.9% in February, having contracted by 0.2 ppts since October last year. Likewise, the job-to-applicant ratio improved to 1.1x in the same month, although this may be masking the full extent of the damage from the pandemic.

According to Nomura Research Institute, unemployment rates, including those effectively unemployed, are estimated to be a few percentage points higher. The Tankan survey of March 2021 shows a marked improvement from the December survey but suggests a K shaped recovery.

Logistics remains the most sought-after sector and valuations have reached new highs, while multifamily as a stable defensive play remains popular, particularly among international investors. Regarding office space, demand for well-located value-add opportunities is firm, but some investors find the outlook uncertain. Tough times persist for retail and hospitality and COVID-19 infections are likely to linger. There are still few distressed opportunities being offered in the market and securing new loans for these sectors could be challenging.

We currently observe stronger demand for Japanese real estate from overseas. In fact, on 2 April, Starwood Capital Group announced their intention to conduct a takeover bid for the Invesco Office J-REIT. This demonstrates that a wider range of parties appear more optimistic about the Japanese office market.

The TSE J-REIT index was up a promising 12.9% over the quarter but remains around 10% below pre-pandemic levels achieved in February 2020. The recovery of the hotel sector has been priced-in while the underperformance of offices appears to have corrected. The TOPIX index has stood comfortably above pre-pandemic levels since mid-November, recording 2,013.71 at the end of March, marking a 30-year high.

The BOJ conducted its policy review in mid-March and yields on 10-year government bonds are now allowed to move between -0.25% and 0.25%, a slightly wider range. It has also dropped its target for annual ETF purchases, implying that it remains willing to intervene, but only when necessary. The review appears to have made monetary policy more sustainable.

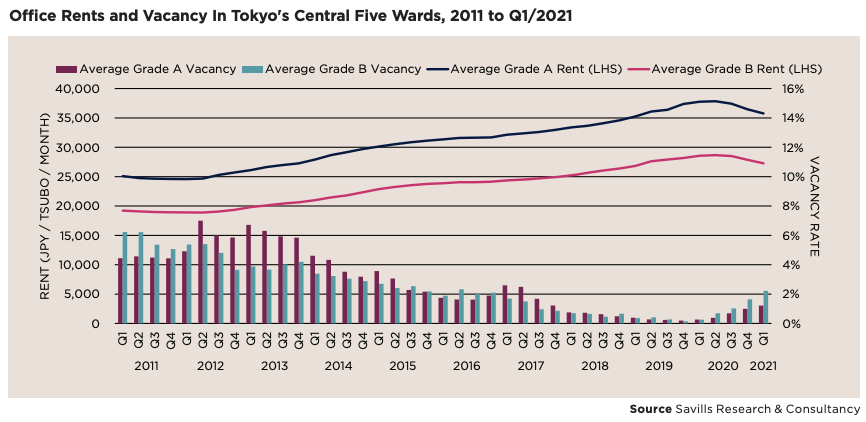

Within the Tokyo central five wards, Grade A office market vacancy rates have increased slightly to 1.2% in Q1/2021. Meanwhile, rents have fallen by 1.9% quarter-on-quarter and 5.3% year-on-year, and now stand at JPY35,762 per tsubo per month. With limited supply expected this year and next, the market should have time to adjust and recover, although secondary vacancy derived from the elevated supply levels in 2020 is still a concern.

Advertise

Advertise