Why Tokyo’s prime retail market is set to enjoy accelerating capital value growth

Rental growth is a significant contributing factor.

After suffering from the effects of the pandemic, the prime retail market in Tokyo is finally recovering. According to a JLL article, consumption momentum continues to strengthen as pent-up demand from domestic consumers in particular is released.

“Luxury goods saw the strongest growth during Jan-May 2023, with sales increasing by 40% as compared with the same period in 2019 before the pandemic (Japan Department Stores Association). Increased tenant confidence is underpinning increased inquiries for new openings,” says JLL’s Naoko Iwanaga.

Here’s more from JLL:

Capital values in Tokyo’s prime retail market fell during the pandemic (-19% compared with 4Q19 based on JLL data), because of changes in rents and cap rates (-11% and +20 bps, JLL data). Capital values bottomed out in 2Q21 and resumed growth thereafter, with upward momentum accelerating in 2Q22 in line with strong rental growth to date.

Ground floor rents have led rental growth. By submarket, Ginza is approaching 2019 levels with unit rent of JPY 275,000 per tsubo per month (preliminary 2Q23, JLL data), while Omotesando exceeded 2019 levels, with a historic high of JPY 245,000 per tsubo per month in the quarter (Figure 1).

Rental growth is underpinned by the more favourable balance of demand and supply. With strong demand for high-quality space coming from luxury brands in particular, supply options that meet their requirements is extremely limited. As such, prime retail properties are reportedly seeing intense competition upon tenant turnovers.

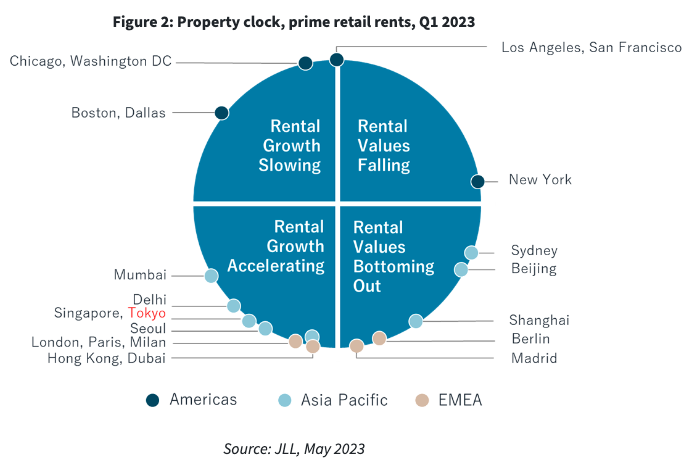

Looking ahead, Tokyo’s prime retail is expected to see accelerating capital value growth, partly driven by rental increases as implied in the current position of the retail property cycle (Figure 2).

In addition to accelerating ground floors, demand from F&B operators can add momentum to the upper floors upon the full return of footfall of both domestic (railway passenger numbers in broader Greater Tokyo in February 2023 recovered to 83% of the same month in 2019, MLIT) and international (foreign visitor arrivals in Japan in May 2023 were 67% compared to the same month in 2019, JNTO).

Possible cap rate compression will also drive increasing capital values

Cap rates are expected to compress or remain stable at least. Retail investment activity virtually halted during the pandemic, reflecting the investors’ wait-and-see approach and the owners’ confidence in the long-term value, but has been increasing recently, with notable transactions including those relating to small-lot Specified Joint Real Estate Ventures (Fudosan Tokutei Kyodo Jigyo: FTK). The appeal of the FTK financial instrument, with the property located in the prime streets including Ginza and Omotesando, to high-net-worth individuals (HNWI) and their asset management companies is such that the product would often be sold out in a short time.

Typically, direct or indirect real estate investment by HNWIs and their asset management companies place emphasis on the prime location as they prioritize more the asset value in the long-term and less the income, and so cap rates tend to be lower than the market. The increasing presence of HNWIs is having impact on the pricings of traditional players including institutional investors, real estate funds and J-REITs, placing downward pressure on cap rates.

Tokyo’s prime retail market is recovering from the disruption of the pandemic, attracting consumers with goods and services. Prime retail properties both offer a place for retail and F&B businesses to thrive, and also appeal to diversified investors seeking sustainable income and value growth.

Advertise

Advertise