Singapore non-landed home prices up 4.1% in Q3

This is due to the new price benchmarks set by projects in the OCR.

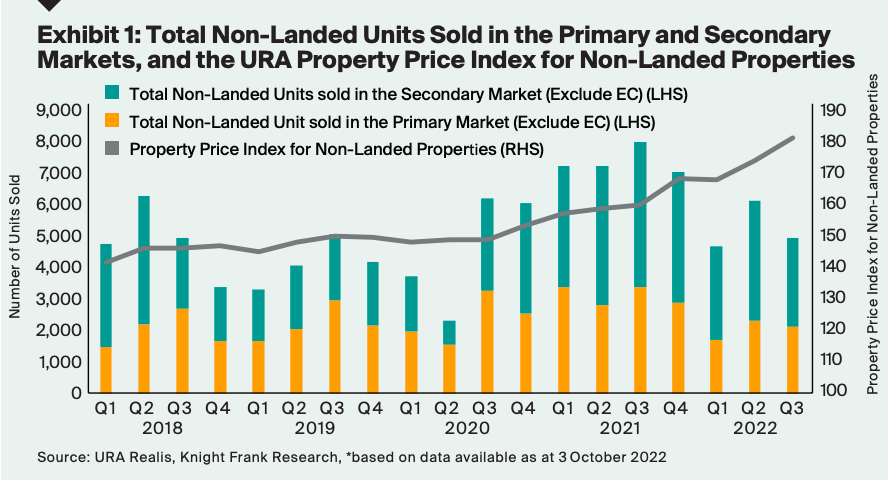

Singapore’s non-landed private home prices (excluding Executive Condominiums (ECs)) rose by 4.1% q-o-q in Q3 2022**, chalking up a cumulative increase of 7.5% in the first nine months of 2022.

According to Knight Frank, the rise in prices was mainly due to headline project launches in the Outside Central Region (OCR) setting new price benchmarks for suburban condominiums.

Here’s more from Knight Frank:

However, the total volume of non-landed private transactions declined by 18.7% q-o-q, with 4,963 units in Q3 2022* as sentiment turned reticent with growing worries over inflation, rising interest rates and fears of an impending recession.

New sales shrank by 7.9% q-o-q in Q3 2022* with 2,143 units sold. Sales in the secondary market decreased by 25.4% q-o-q with 2,820 transactions recorded in Q3 2022*. In the resale market, the inventory of saleable stock narrowed as potential sellers anxious over procuring suitable replacement units in light of escalating rents in the leasing market, increasingly adopted a watch-and-wait posture. In a climate where there were more buyers pursuing the diminishing pool of ready-to-move-in units, prices grew across all regions while transaction volume shrank.

Core Central Region (CCR)

Prices of non-landed homes in the CCR increased 2.3% q-o-q in Q3 2022**. The proportion of non-resident homebuyers in the CCR also grew from 9.0% in Q1 2022 before air travel lanes opened in April, to 11.1% in Q3 2022*. Slightly more High-Net-Worth-Individuals (HNWIs) purchased private homes for both owner-occupation and investment opportunities in the CCR notwithstanding the Additional Buyer’s Stamp Duty (ABSD) for foreigners.

Nevertheless, the total non-landed transactions in the CCR contracted by 9.7% q-o-q to 1,085 sales in Q3 2022*. New sales in the CCR decline by 5.3% q-o-q with 539 sales recorded in Q3 2022*. In tandem, transaction volume in the resale market declined by 13.7% q-o-q to 546 sales in Q3 2022*. The fall in non-landed private home sale transactions in the CCR was mainly due to the lack of new projects launched coupled with the limited availability of family-sized units in the resale market.

Rest of Central Region (RCR)

Prices of non-landed homes in the RCR increased 2.5% q-o-q in Q3 2022**. The easing of price gain was likely a result of no new launches in the region, as a substantial number of units at Piccadilly Grand and LIV@MB (both launched in Q2 2022) have been sold.

Total transaction volumes in the RCR declined by a considerable 50.8% q-o-q to 1,222 sales recorded in Q3 2022* as there were no new launches. Sales volume in the secondary market dipped 28.5% with 856 transactions recorded in Q3 2022*.

Outside Central Region (OCR)

The OCR was the most active region in Q3 2022 with the price index for non-landed homes reaching an all-new record high, as prices increased 7.0% q-o-q and surged of 18.1% y-o-y in Q3 2022**. The hike in prices was due to several new launches that captured the attention of mostly Singaporean homebuyers.

Overall sales in the OCR increased by 9.8% q-o-q recording 2,656 sales in Q3 2022* due to the strong take-up rates of 98.0%, 84.0% and 75.0% that were recorded for AMO Residences (total of 372 units), Lentor Modern (total of 605 units) and Sky Eden@Bedok (total of 158 units) respectively when these new projects were launched.

There remains ample demand from homebuyers comprising both HDB upgraders as well as new family formations whose housing aspirations remain high.

Rental movements

Island wide rental contracts for non-landed private homes totalled 16,389 in July and August 2022, a significant increase of 24.5% in comparison to April and May 2022, but 7.0% lower than the same period last year. Rents increased between 3% and 10% q-o-q across the various market segments with competition from lessees expected to continue.

The opening of borders coupled with the introduction of employment policies to attract top talent worldwide would increase leasing demand from professionals drawn to a stable Singapore, adding to the local residents who have been unable to find a suitable replacement home. Private residential rents are projected to continue trending upwards in the remainder of 2022 and well into 2023 until the bulk of the expected 17,000 plus new private homes are completed next year, providing much needed housing.

Market outlook

The most recent announcement of the cooling measures that took effect from 30 September 2022 will impose a wait-out period of 15 months. Downgraders from private homes, including retirees, would now have to source for alternative accommodation before being eligible to buy a non-subsidised HDB resale flat that is larger than a 4-room unit.

This group would likely either rent or stay with relatives or friends. Those who do not have options other than to rent would exacerbate demand in the leasing market, putting more upward pressure on private residential rental values that have already been increasing substantially throughout 2022. Rents in the private residential market will continue to increase in the remainder of 2022 and into 2023.

Notwithstanding the latest round of cooling measures, homebuyers who are still on the lookout for a new home that is under development and hope to make a purchase before interest rates increase further, will likely continue to be active at launches in the remaining months of the year. Overall, private residential prices have now swelled beyond the earlier expectation of 5% to 7% for the whole of 2022, and will now likely end 2022 with about 10% gain.

However, the mix of cooling measures just nine months apart, a possible recession in 2023, widespread inflation, and the manner in which private home prices have climbed in the last two-and-a-half years, will inevitably start to shift the sentiment of some homebuyers into tentative territory as interest rates progressively rise from now and into 2023.

* based on data available as at 30 September 2022. Figures exclude Executive Condominiums (ECs).

** based on flash estimates announced on 3 October 2022.

Advertise

Advertise